6 min read

Aug 14, 2025

How SBA loans serve US Small Business today

SBA loans are a great product for small businesses because the government guarantee brings down the cost of capital, making it typically the most affordable way to borrow money.

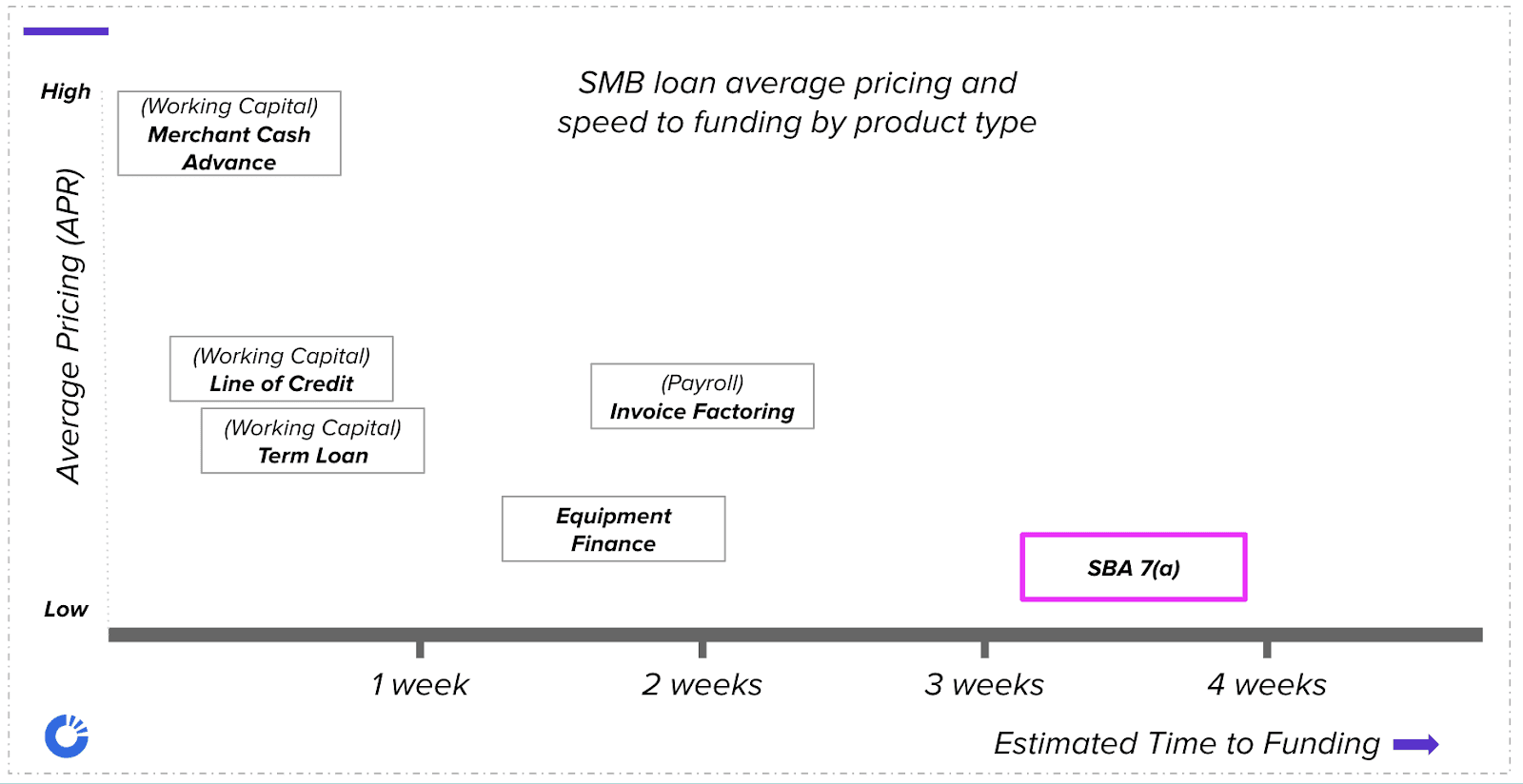

The guarantee does come with a lot more paperwork and processing time than comparable non-guaranteed loans though, making it difficult to get for a lot of small businesses.

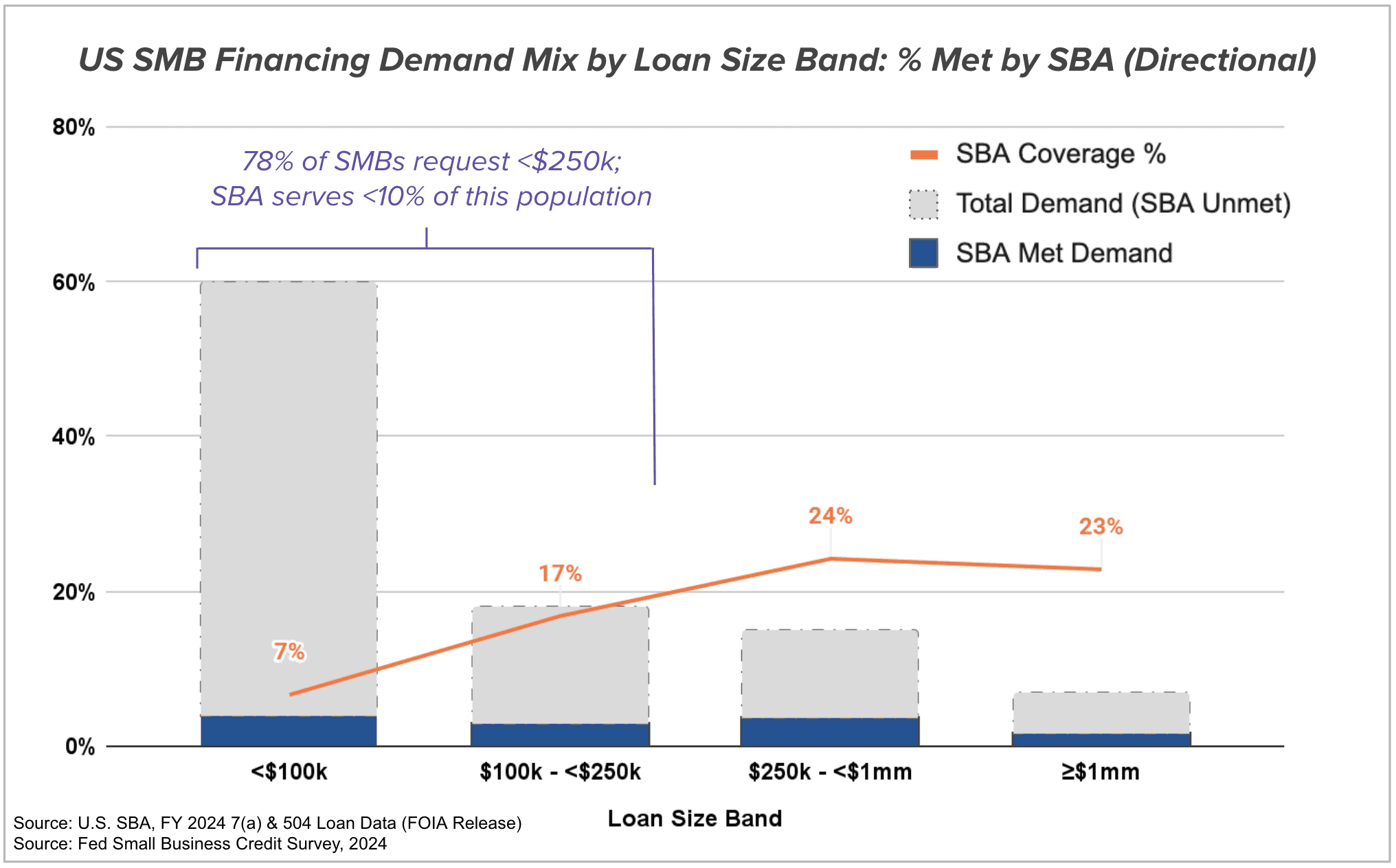

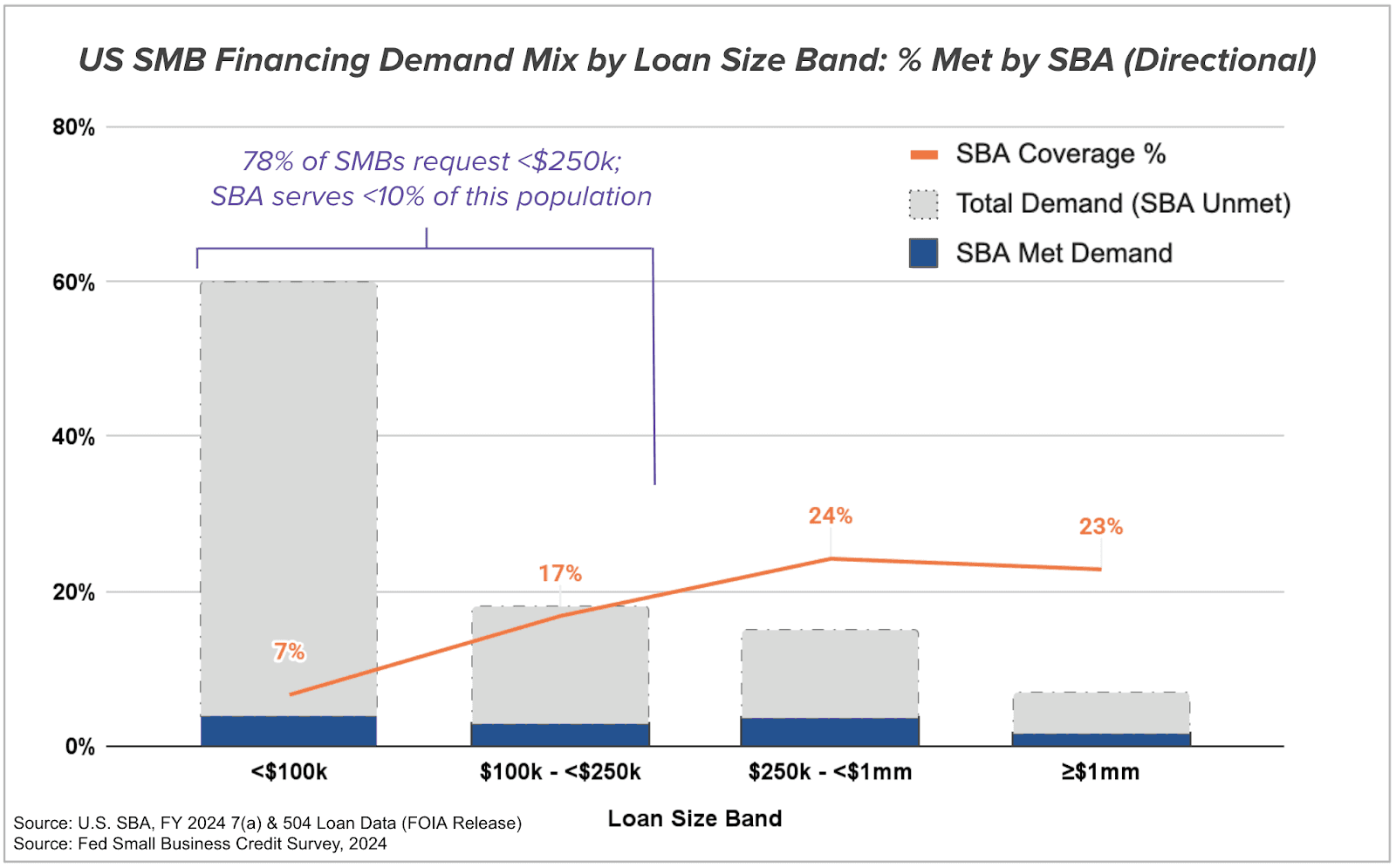

The result is that the average SBA 7(a) loan is nearly half a million dollars, and the average SBA 504 loan is over a million dollars, even though 78% of SMBs only request $250k or less; it’s typically only worth it for borrowers and lenders alike to go through the whole SBA process for larger loans.

For borrowers, the months that SBA loans can take is too long; over half seek financing to meet operating expenses and manage cash flow so it’s only worth sticking it out for a larger loan

For Lenders, the cost of originating a smaller SBA loan today is often the same as a larger one, so taking into account limited team capacity and the higher loss rates on small loans, it's no wonder lenders prioritize larger loans

This creates a pretty big mismatch between the loan sizes borrowers are seeking vs SBA loan sizes. To be clear– SBA loans are not a fit for every small business need. There are bonafide reasons other structures like line of credit make more sense for some short term cash flow needs. And not everyone has the strong credit (e.g. mid-600s+ FICO) needed for SBA either. That being said, I believe the gap today far exceeds these scenarios, and there is tremendous opportunity for SBA lenders to sustainably grow their programs by helping really good small businesses that happen to only need lower ticket sizes.

So how do we expand access to the best SMB loan product in America?

This is a question we thought deeply about during my 7 years at Funding Circle, where our average loan size was more aligned with borrower requests in the $100k-$200k range, and, driven by tech and streamlined operations, our time to funding was just days instead of weeks or months.

In 2023 the SBA made some of the biggest changes to the program in over 40 years, including the “Do What You Do” language - allowing lenders to follow their own existing credit policies for <$500k loans rather than the complex SBA ones - as well as granting three new SBLC licenses (allowing a non-bank to originate SBA loans). Funding Circle applied for a license with the vision of bringing its smaller loan expertise to the SBA market to help fill this sub-$500k gap, while also lowering the cost of capital, and was awarded one of the licenses.

Fast forward a couple years and a lot has changed. While this vision continues to some extent at iBusiness Funding as a Lender Service Provider for Ready Capital, after acquiring Funding Circle’s US operations in 2024, 2024 was also the first year the SBA program had negative cash flow for over a decade.

There is a sense in the community that the “Do What You Do” change implemented in 2023 contributed to an increase in defaults and unprofitability in 2024, and in June 2025, the language was removed from the SBA Standard Operating Procedure (SOP). If you ask an SBA lender which exact rule in the ~500 page SOP has been protecting the program from 2024-style losses in prior years, you might not get an exact answer, but there is a sense that collectively - explicitly or through selection - they have achieved this outcome, even if while adding friction to the borrower experience.

Credit Conversion vs Borrower Conversion

In lending we talk about “credit conversion” vs “borrower conversion.”

Credit conversion is all about the lender saying “yes” to applicants, passing eligibility tests, and ultimately underwriting

Borrower conversion measures the borrower actually submitting the information and documents needed for the eligibility checks and underwriting

Together, they represent the portion of all applicants that end up getting funded. At Funding Circle, surprisingly half of the dropout was not due to credit declines, but rather just due to applicants failing to submit all the necessary information. And this was for a process that was far more streamlined than SBA.

The 2023 SBA changes took a pretty ambitious crack at increasing Credit conversion, but with lending this is always tricky and risks backfiring in the form of higher defaults / loss rates (as it did in 2024).

Looking forward, at OmniAI we believe the next phase of SBA optimization will come instead from Borrower conversion, which while harder to influence up front, is less fraught with downstream loss increases.

Why borrower conversion is the biggest opportunity in SBA lending

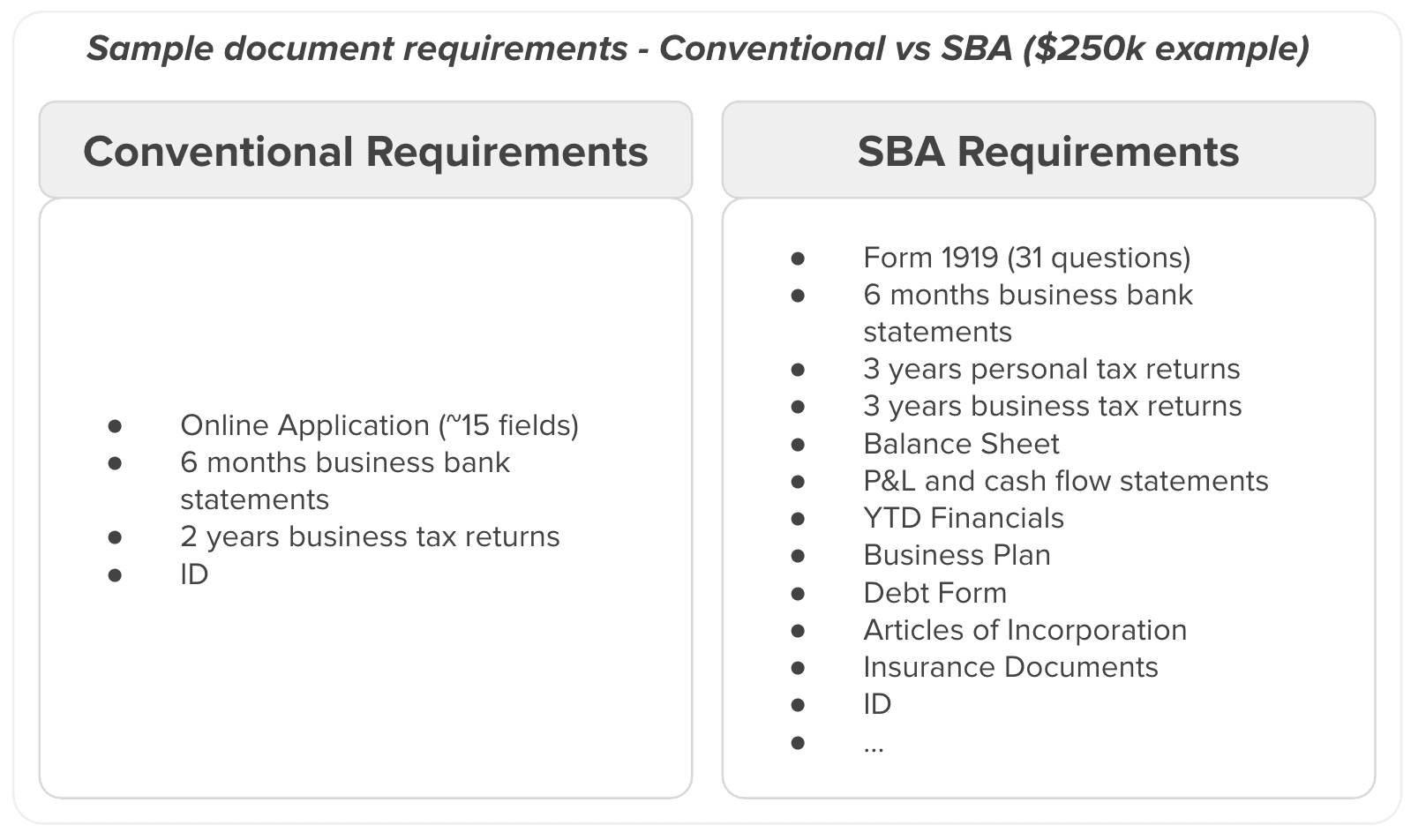

The reason SBA loans take so long and have so much borrower dropout is the extensive document requirements (see below illustration), which is also what makes the smaller loans less profitable for lenders.

Each document takes a long time to furnish, and often after the lender checks it, it turns out a different, revised, or additional document is required as well. Imagine you accidentally submit a personal bank statement instead of a business one! And the lender doesn’t even realize for a couple business days…

This back and forth takes multiple business days each time, especially if you take into account that the small business owner is juggling many tasks running their business besides just administrating a loan application process, day to day.

This is where automation can come in. AI agents can correspond with borrowers to collect all the documents, crucially responding in seconds each time the applicant provides an input, to keep momentum up in the application process: if changes or clarifications are required, the applicant finds out in seconds instead of days.

While we see many opportunities for this technology to make a difference across a wide variety of complex customer onboarding experiences, SMB lending and especially SBA lending present some of the most attractive customer pain points to address, both in terms of how much AI can help and the end impact it can have.

The opportunity in front of us

Small businesses create 2 out of 3 new jobs in America and play an outsized cultural role in the communities they serve, hiring and hosting their neighbors. It’s time we stepped up and helped them secure easier access to affordable capital. There’s never been a more exciting time to leverage technology to work on this.

Last week the OmniAI team was onsite at the America East conference in Atlantic City, to spend time with one of our core verticals– SBA lenders. We had a lot of good conversations but one theme emerged above the rest: how can we scale operations to increase access, without sacrificing program stability?

At the conference, we were thrilled by both the shared passion to help small business, and the interest - all the way up to the SBA - in how AI can play a role. If you’re thinking about streamlining the borrower experience with AI, we’d love to collaborate.